Introduction

On March 13th, 2020, the United States economy nearly grounded to a halt.

With the World Health Organization’s declaration of COVID-19 as a global health pandemic, President Trump’s announcement of travel bans on China and Europe, and American businesses revising guidelines and practices all within a short time span, American life changed dramatically. In March alone, the New York Stock Exchange momentarily suspended trading in response to sudden steep falls in the value of the DOW Jones and S&P 500 on four separate occasions. Multiple airline companies signaled their need for federal bailouts, while retailers such as JCPenny and JCrew filed for bankruptcy. On the ground, nearly 15 million Americans filed for unemployment only days after the government enacted social distancing measures and by May, the official unemployment rate reached around 15%. Anecdotal evidence of frustrated Americans waiting for hours or even days on hold to speak with an unemployment benefits representative has become commonplace. All the while the contagion spread, infecting over 1.7 million and killing over 100,000 of our fellow Americans before the end of May.

It is nearly June and the economic picture of the future appears tentatively optimistic. States and counties are moving to lower threat levels, governments and businesses are easing social distancing guidelines, and many parts of American life are slated to return after being unavailable for months, albeit with new and more stringent health guidelines.

“Consumers’ confidence in the economy is currently low, and it will take effort to revive it. ”

And yet the shift “back to normal” will not be nearly as abrupt as the move to life under lockdown was. For all their efforts, governments and businesses may have to work hard to coax the American people back to work and back to their normal spending habits. Consumers’ confidence in the economy is currently low, and it will take effort to revive it.

There are at least two reasons for this. First, many American consumers will have reservations about returning to business as usual, especially to mass gatherings and other events that pose high risks of community transmission. Due to the nature of the outbreak, returning to normal will be much more complicated than simply flipping on a switch, and some forms of less intensive social distancing will need to remain in place for many months yet. One expert referred to this timetable as “The Hammer and the Dance,” noting that maintaining some form of social distancing even after new cases peak can save lives. In a simple framework of the economy as a supply side and demand side interaction, the supply side is now eager to revamp production again, but the demand side waits cautiously.

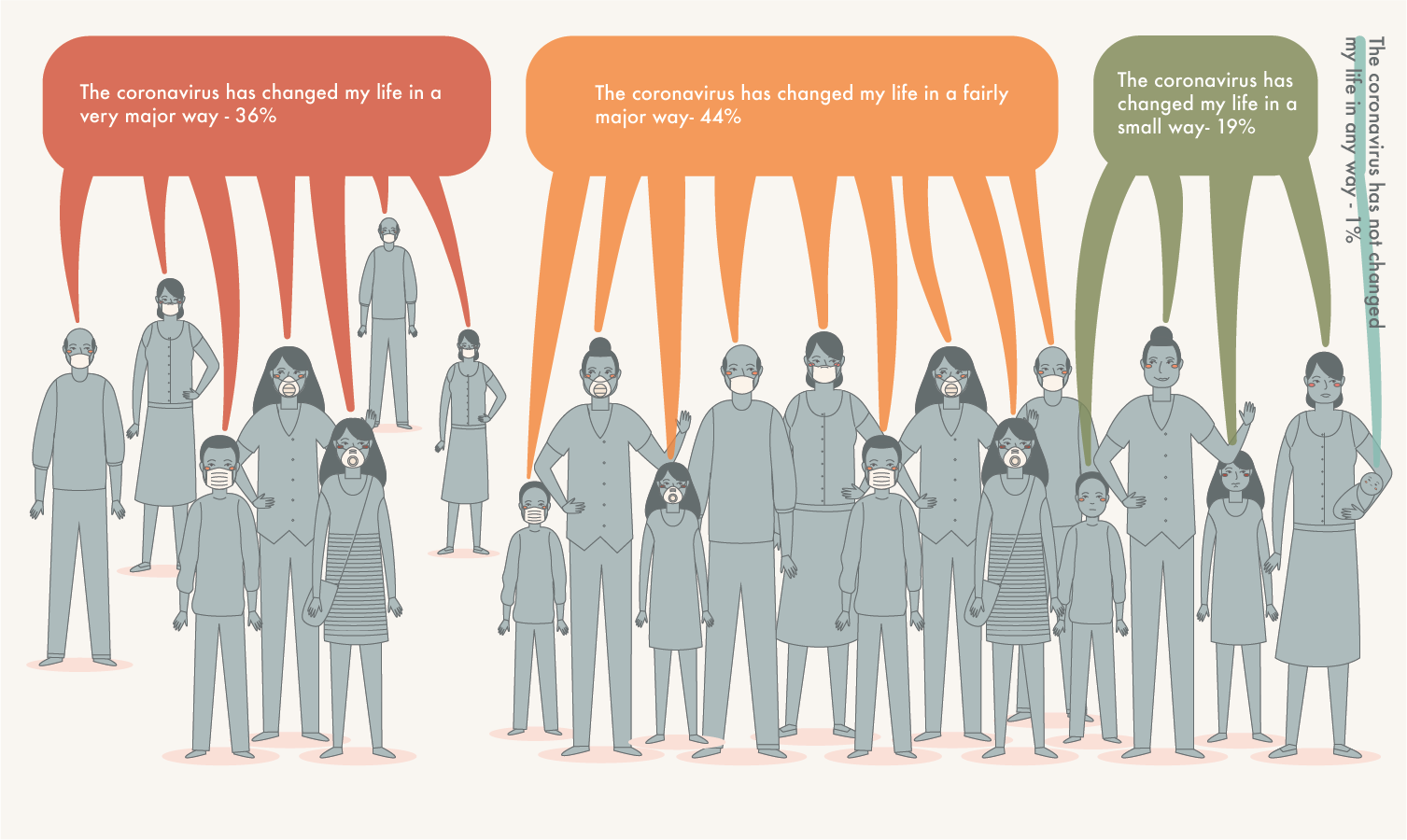

Second, certain subsets of Americans are markedly less fit to cope with this pandemic than are others, or at least feel so. The virus itself aside, social distancing measures have not affected everyone equally, with certain groups of people experincing significant financial setbacks making them less optimistic about their financial future.

Here, we focus on this second phenomenon: that social distancing measures inevitably have unequal effects on different groups in American society. Some have postulated that the long-term effects of social distancing measures will depend upon one’s income, gender, age, and a number of other factors. We are especially equipped to analyze these distinctions among Utahns using public opinion data that we have collected. Our respondents’ sentiments can give us insight into how a broad spectrum of people are feeling about the foreseeable future under the coronavirus, both here in Utah and across the nation.

Overall Results

The vast majority of respondents consider the US to be worse off than it was six months ago, which is certainly to be expected. 79% of total respondents believe that the US’ economic state has worsened in recent months, while only 11% of respondents report that the economy has improved. While most respondents believe that the US is in worse shape, respondents’ individual financial situations do not necessarily reflect the overall US expectation. A slight majority of respondents report that they and their families are doing about the same financially as they were six months ago. However, more respondents are reportedly worse off financially than are better.

When questioned about their expectations for the future of the US’ economy, respondents are, for the most part, optimistic. A slight plurality of respondents (43%) believe that the economy will improve, followed closely by 38% of the sample believing the situation will worsen. Nearly half of respondents expect that their personal financial situation will remain the same, which seems to reflect the report that respondents, as a majority, were financially unaffected by the outbreak. The other half of respondents were essentially equally split on whether they would be better or worse off in the coming months.

Results by Selected Demographics

As one might expect, nearly all respondents, independent of income, are in agreement that the United States is economically worse off than it was six months ago, with all income groups approximating the total average of the sample (around 79%). Interestingly, those respondents in the highest income bracket of the sample (individuals that earn over $100,000) have the highest proportion who consider themselves financially worse off compared to middle- and lower-earners. On the other hand, lower-earning respondents were the least likely to consider themselves better off between all three subsets.

High-earning individuals are the most pessimistic about the US’ economic future among earners. Analyzing the weighted data, a plurality of respondents that expect the economy to worsen come from those in the highest income bracket. On the other hand, the number of high-earning individuals that believe the economy will improve in six months is slightly above the number of those that think it will worsen. Low-earning individuals are the most evenly distributed over the spectrum, with nearly equal percentages of respondents from that subset equally represented in each response. These lower-earning respondents were the most likely to choose “about the same” among the income demographics. They were also the least optimistic that the US would improve economically. Lower-earning individuals are the most pessimistic about their own personal financial future, more so than their higher-earning counterparts. A plurality of all respondents across income brackets expected to be “about the same” financially in six months. All income groups approximated the sample average of 27% in their belief that they would be better off in the near future.

Men generally believe that the US is doing better than women do. While both sexes as a majority believe that the country is worse off, men were as a whole less likely to report that the US is worse off. Men and women are essentially even in their estimations of how their families have fared financially over the past six months, with the slight majority of both sexes reporting that they are “about the same.” When thinking about the future of the US’ economy, women are more likely to be pessimistic about the next six months. Far less women than men, percentage-wise, are likely to believe that the US’ situation will improve, and are more likely to estimate that the US will be worse off in the coming months. This pessimism carries on to respondents’ personal expectations of their own financial well-being. Men are more likely to respond that they will be better off, while women are less likely to do so, and more likely to expect that they will be worse off.

The older the respondent’s age, the less likely they are to consider the United States worse off than it was six months ago. Those in the younger half of categories for age (18-44) are the most likely to believe that the US is worse off, while the older demographic is more likely to believe that the US has done better recently. Interestingly, the same older demographic reports that they personally have done worse financially in the last six months, more so than the younger respondents reported. A plurality of all respondents report that they have done about the same, although younger individuals were more likely to do so.

Looking to the future, the older generation is once more the most optimistic about the US’ economic potential, while the 18-34 years-old demographic is the least optimistic, reporting the highest percentage among demographics that they expect the situation to worsen. Reflecting their current financial situation, respondents report that they expect their finances to stay about the same as it is in the next six months. More individuals are optimistic that their situation will improve compared to how they have done in the past six months, but for the most part, respondents are confident that they will do about the same.

Conclusion:

In our respondent pool, notably few people disagree that the coronavirus has adversely affected the American economy and their own households’ financial stability. The vast majority of respondents are in agreement that the US is worse off financially than it was six months ago. An overwhelming majority of respondents regardless of age and income similarly report having been personally affected financially by social distancing measures.

However, future expectations differ slightly among demographic groups. In general, lower-income and younger-aged respondents are notably more pessimistic about their own financial futures, as are women. This suggests that while these respondents all feel affected by the pandemic, certain of them feel better equipped, by their own account, to recover from the pandemic financially.

In various news media outlets, COVID-19 has been coined “The Great Equalizer”, an accolade meant to remind us that the virus can spread to almost anyone with very little discrimination. While this is generally true of the virus itself, our results have shown that respondents of different incomes, genders, and ages are markedly different in their worries and expectations of how they will be faring financially six months from now and in the distant future in life after lockdown.